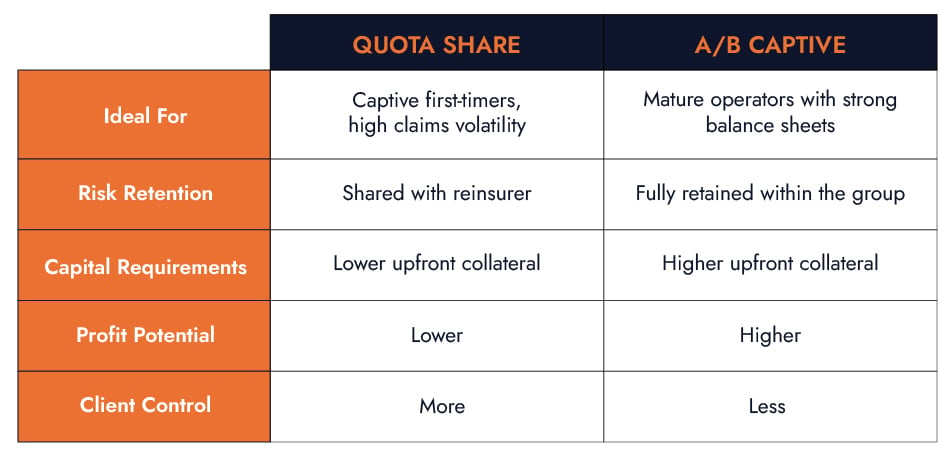

Which One Fits Your Client?

Here’s a simplified breakdown to help you match the structure to the right client profile:

What Agents Need to Know

Captive structures shouldn’t be a mystery. Here’s what you need to understand to explain them effectively:

Collateral:

Quota Share = Less upfront. A/B = More skin in the game.

Assessments:

Only a factor with A/B if the frequency fund gets burned through.

Underwriting Profit:

A/B offers higher upside if the client can manage losses.

Client Readiness:

Don’t force-fit a structure. Quota Share is a great ramp. A/B is better for clients already managing risk well.