Many insurance agents are hesitant to discuss captive insurance with their clients, often due to uncertainty or a lack of familiarity with this alternative. While traditional insurance is straightforward—where a business pays a third-party insurer to assume the risk—captives introduce a level of complexity that can initially seem intimidating.

However, as premiums continue to rise and clients grow increasingly frustrated with limited control and transparency, understanding captives could be a valuable addition to your tool kit.

At Captive Coalition, our sole mission is to help independent agents protect their best clients using captive insurers. We educate agents on the intricacies of captive insurance so they can retain their best and largest clients. With our experience, we know what it takes to understand captives and help you communicate the advantages and disadvantages to your clients.

This article will cover the fundamentals of captive insurance, explain how it differs from traditional insurance, and introduce the various types of captives available.

The 101: What is Captive Insurance?

Captive insurance is a form of self-insurance where the insureds, or a group of insureds, own and control the insurance company. Unlike traditional insurance, where a third-party carrier assumes all the risk, a captive allows businesses to retain some of the risks and benefit from the profits.

Essentially, captives are about taking control: the business invests in creating an insurance subsidiary (the captive) that provides coverage based on their unique risk profile.

How Captive Insurance Differs from Traditional

Captive insurance offers advantages over traditional insurance by giving businesses more control and flexibility. Here’s how:

- Customization: Captive policies are designed to fit a business’s specific risk profile, avoiding the gaps that often come with one-size-fits-all traditional policies.

- Profit Retention: When claims are low, the profits remain within the captive, benefiting the business rather than an external insurer.

- Enhanced Risk Management: Businesses with captives can enforce their risk mitigation strategies more effectively, creating a safer environment and potentially lowering costs.

- Stability: Captives provide consistent coverage and pricing, allowing businesses to plan long-term without worrying about sudden changes in premiums or coverage.

Major Types of Captive Insurance Companies

Captive insurance comes in various forms, each suited to different business needs and minimum premium requirements:

- Pure (Single-Parent) Captives: Owned by a single company, this type insures only the risks of its parent and affiliated businesses. Large companies that typically spend at least $1 million in premiums fit into a single-parent captive.

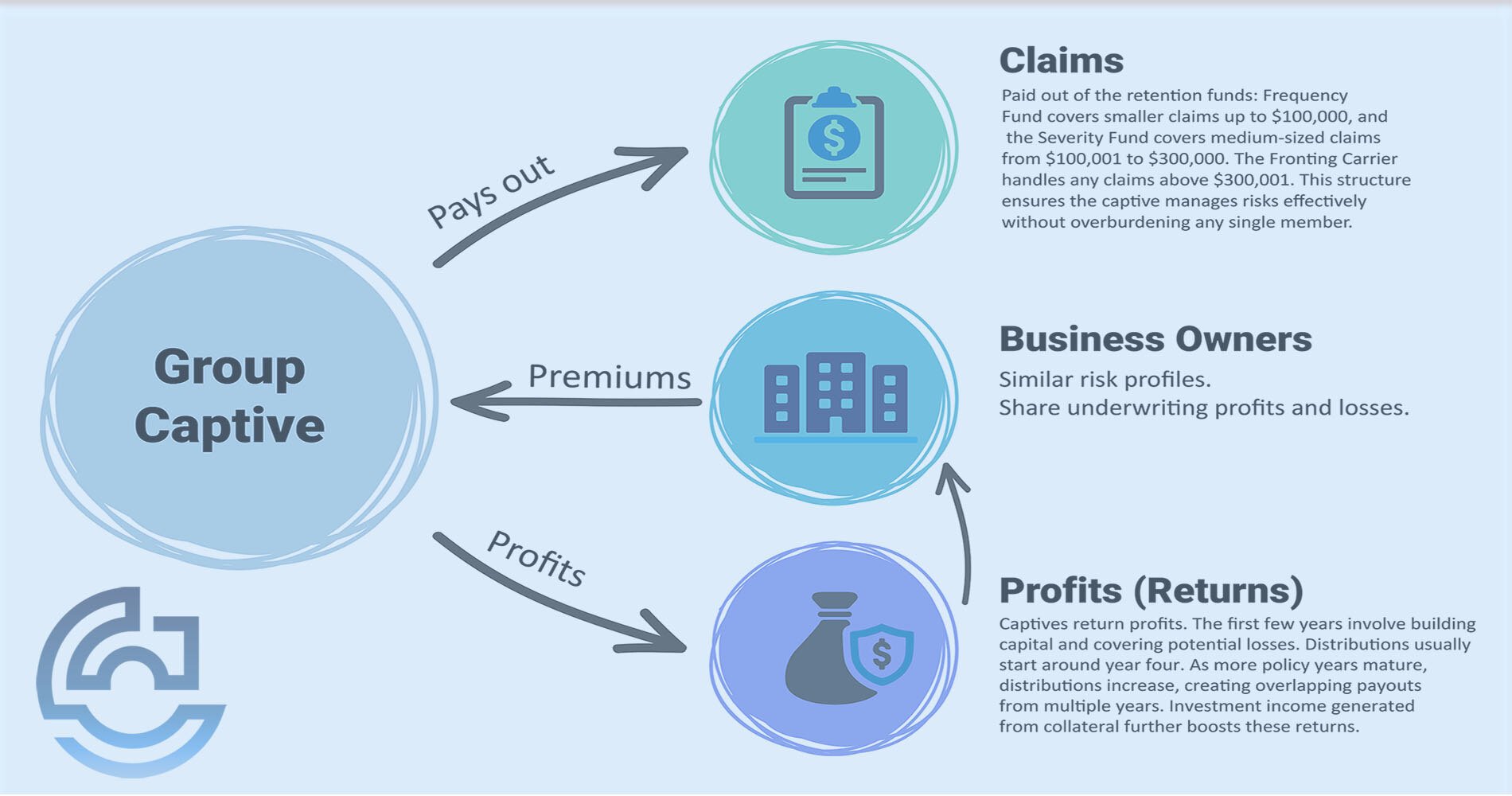

- Group Captives: Multiple unrelated businesses with similar risk profiles pool resources to form a collective insurance entity. Group captives have gained popularity among small to mid-sized businesses looking to manage rising insurance costs collaboratively.

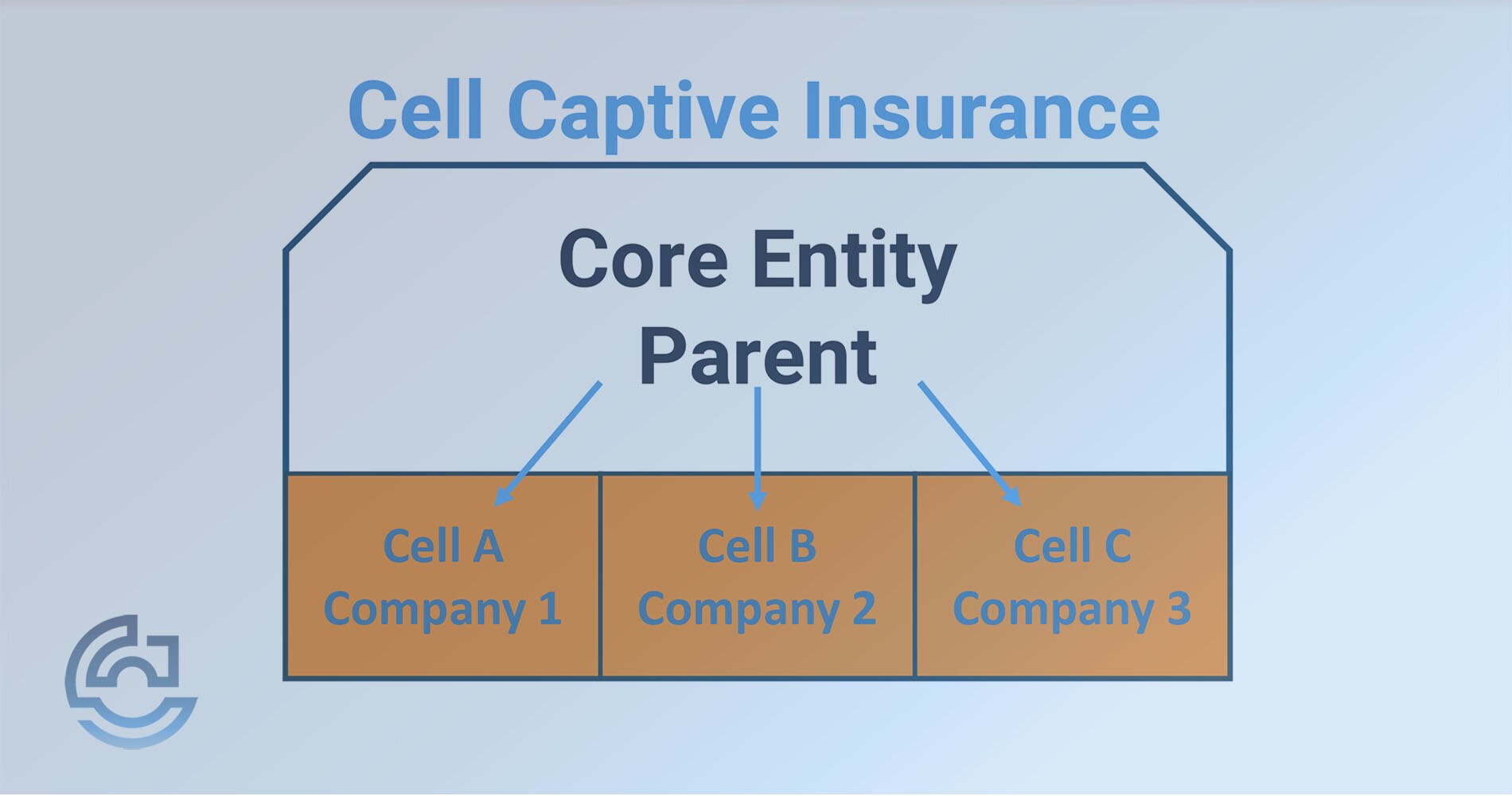

- Cell Captives: These offer a shared insurance structure where multiple entities operate their own “cell” within a larger framework, allowing for risk customization while sharing costs and resources.

- Association Captives: Formed by members of a specific industry or profession, these captives insure the collective risks of the association’s members. They are common in fields like medical malpractice.

The Role of Traditional Insurance in a Captive Program

Despite the benefits of captive insurance, traditional insurance still plays a role in a comprehensive risk management strategy. The ideal approach is often a blend of both, with traditional insurance covering broader, more unpredictable risks, while the captive addresses specific risks that the traditional market might overlook or inadequately cover.

Pros and Cons of Captive Insurance

Pros:

- Cost Savings: Captives can reduce insurance costs over time by keeping profits within the business.

- Control: Businesses have more say in how their risks are managed and insured.

- Transparency: Companies gain complete visibility into how premiums are used with a captive.

Cons:

- Complexity: Setting up and managing a captive requires expertise and commitment.

- Capital Requirements: Businesses need sufficient capital to fund the captive and cover potential claims.

- Regulatory Hurdles: Compliance with regulatory requirements can be challenging and varies by jurisdiction.

Is Captive Insurance Right for Your Client?

Captive insurance isn’t just an alternative to traditional insurance; it’s a long-term strategic insurance tool that can empower businesses with more control, cost savings, and customized coverage. As an independent agent, understanding captives will allow you to offer your clients a potential solution that could dramatically improve their insurance experience.

Whether it’s a pure captive for a large corporation or a group captive for a smaller business, the right captive strategy can offer more transparency, control, and financial benefits that traditional insurance often lacks.

For any other questions on captives or for a consultation, schedule a call with one of our insurance advisors at Captive Coalition.

Topics:

{kind=link}