Many independent agents hesitate to discuss captives with their clients, especially when the subject feels complex or unfamiliar. However, captives offer an excellent opportunity to provide more robust insurance solutions that meet clients' needs.

One option to consider for your clients is group captives. At Captive Coalition, we focus on educating independent agents about captive insurance so they can confidently present these options to their clients.

This article will break down the essentials of group captive insurance. By the end, you’ll understand what a group captive is, how it works, and whether it can be the right solution for your clients. We’ll also cover the mindset and financial stability required for businesses to succeed in a group captive, helping you better serve your clients.

What is Group Captive?

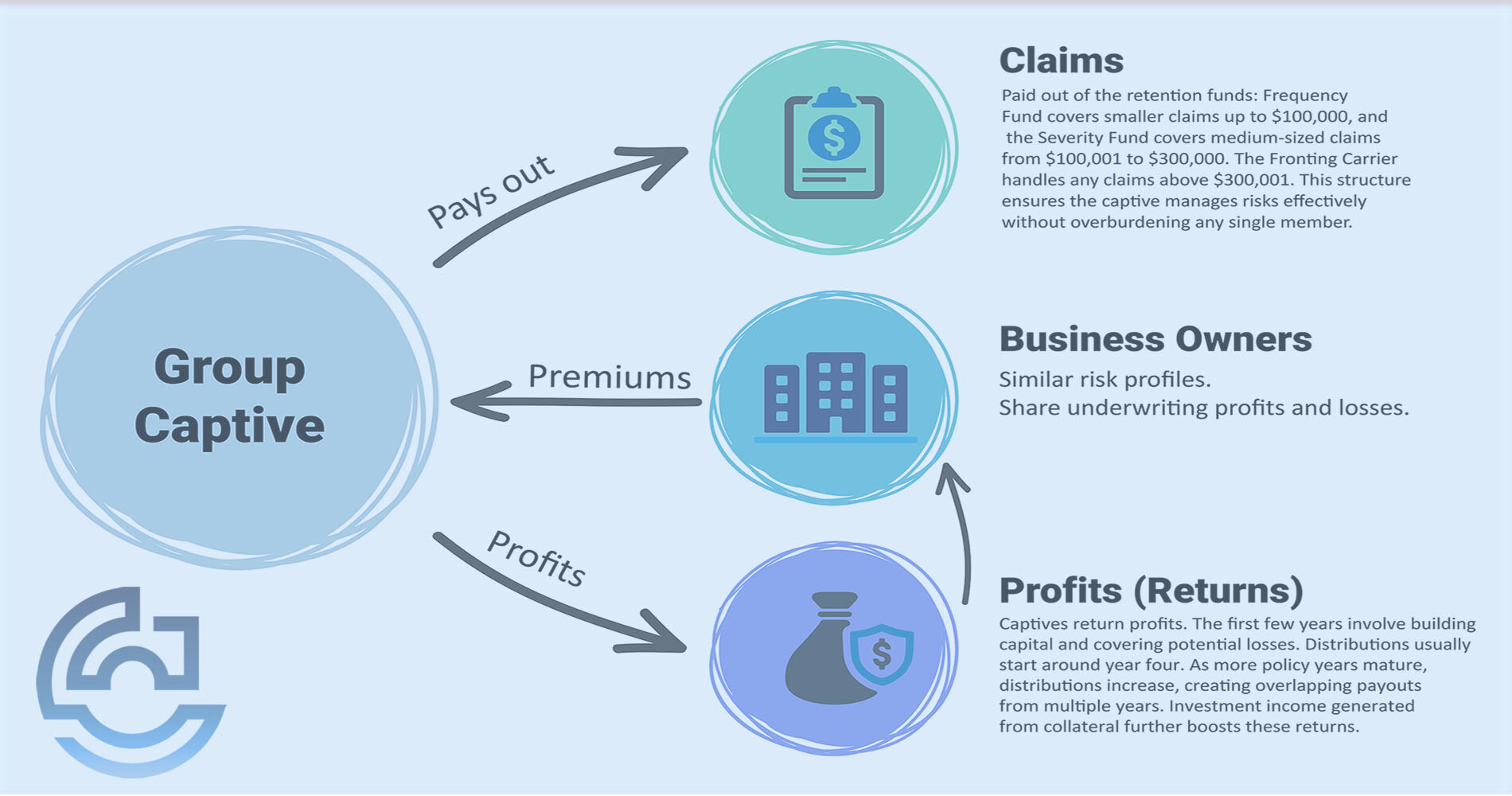

A group captive is a shared insurance venture where similar businesses pool resources to manage and underwrite their risks for control and cost savings. These businesses collectively own and operate the insurance entity, gaining greater control over their insurance costs and improved stability and transparency.

Why Group Captives Work

Businesses in a group captive typically share similar risk profiles. By pooling resources, they can secure more favorable insurance terms than they would individually. Here’s why:

- Pooling of Resources: Sharing resources spreads risk, lowering insurance costs for each participant.

- Control Over Risks: Group members actively manage their risks, resulting in lower claims and more predictable insurance costs.

- Transparency: Unlike traditional insurance, group captives offer complete transparency. Members know precisely where their premiums go and have a say in how funds are used.

Key Qualities of Businesses Suited for a Group Captive

Only some businesses are a good fit for a group captive. To determine if your client could thrive in this environment, consider these essential qualities:

- Entrepreneurial Mindset: Businesses with proactive and innovative leaders who seek better ways to manage risks tend to succeed in group captives. These types of businesses don’t settle for the status quo.

- Commitment to Risk Management: Businesses with solid risk management practices, safety programs, and a track record of minimizing losses thrive in group captives. These companies view insurance as a strategic part of their business.

- Financial Stability: Financially stable businesses with consistent growth are well-suited for group captives. Typically, businesses paying between $250,000 and $5 million in annual premiums are ideal candidates, as they have the resources to invest in a captive and manage risks effectively.

You might be wondering if your clients have these qualities. Become a member of Captive Coalition for free to access help, training, webinars, tools, and resources to better help your clients access captives.

When to Avoid a Group Captive

While group captives offer many benefits, they aren’t for everyone. It’s important to recognize when a group captive might not be the best fit for a client:

- Lack of Commitment: Businesses unwilling to invest time and effort into solid risk management practices may struggle in a group captive. This model requires active participation and a hands-on approach to insurance.

- Financial Constraints: If a business lacks the financial stability to cover upfront costs and potential assessments, traditional insurance may be a better option for those seeking a more passive approach.

Helping Your Clients Make the Best Insurance Decision

When considering a group captive, focus on these key factors:

- Leadership Mindset: Is the business owner entrepreneurial and motivated to take control of their risks? If so, they may thrive in a group captive.

- Financial Health: Does the business have the financial strength to handle the costs of joining and maintaining a group captive?

- Risk Management Practices: Businesses strongly committed to risk management will most likely benefit from a group captive.

Is a Group Captive Right for Your Client?

Understanding group captives can give you an edge as an independent agent, enabling you to serve your clients better. A well-suited group captive can provide your clients greater control, transparency, and financial stability, particularly in markets where premiums rise despite having no claims.

Next, explore another captive insurance model—Single-Parent Captives. Learn more to see if this model is a good fit for your clients. Later, you can compare the pros and cons of single-parent and group captive insurers.

Still not sure if group captives work for your best clients? Prequalify your clients to see if they're a great fit for them.

Topics:

{kind=link}