Many independent agents hesitate to discuss captive insurance, especially when it comes to the different structures available. This can lead to missed opportunities for both agents and their clients. At Captive Coalition, we help you confidently understand and present captives, including the cell captive model.

This article will help you understand what cell captives are, their benefits, and their drawbacks. That way you can present them as a potential option for your best clients.

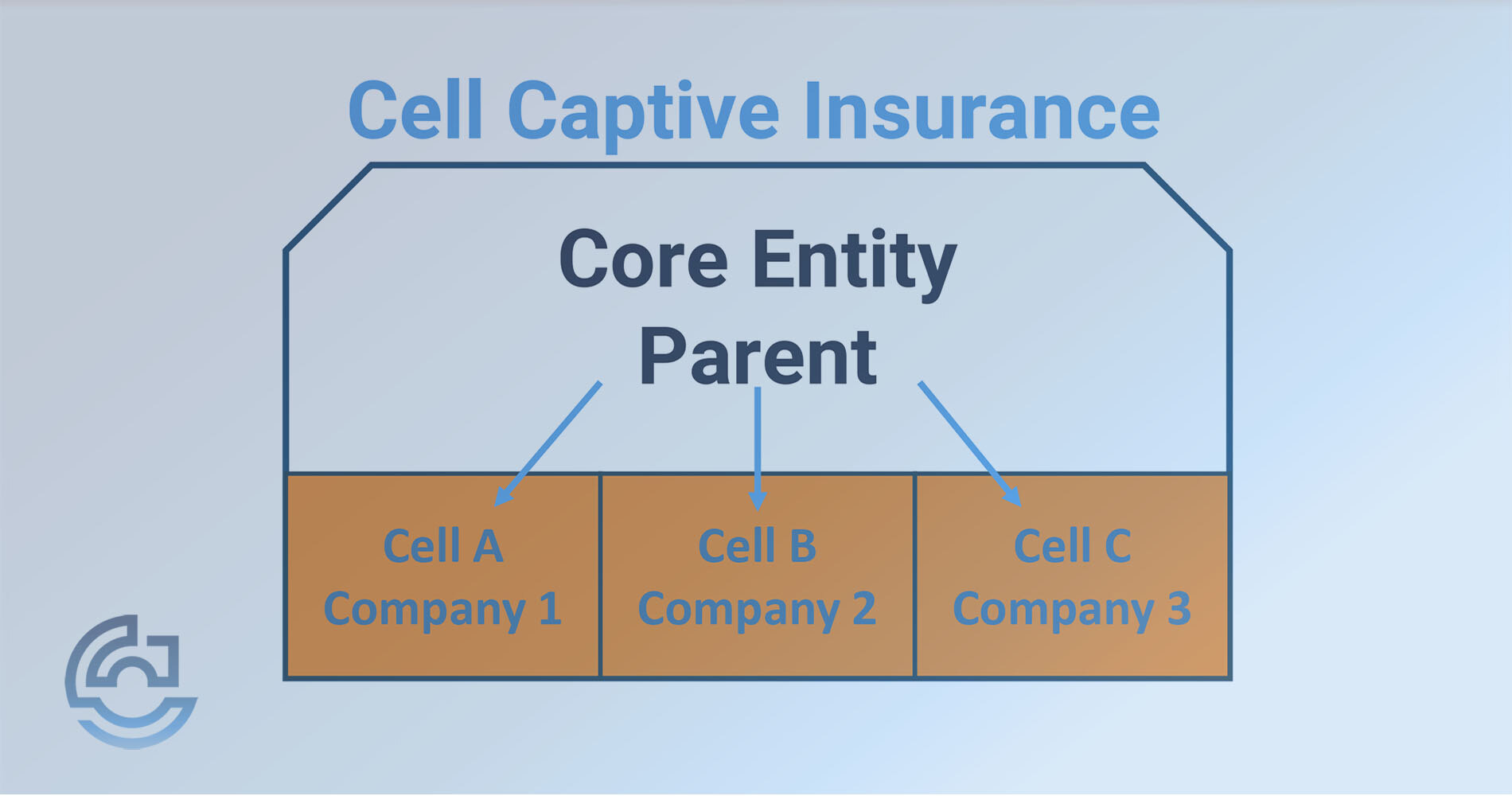

What is a Cell Captive Insurer?

A cell captive is an insurer that allows businesses to share a parent structure while keeping control over their own risks, policies, and finances. This structure allows multiple insureds to share a common framework while also having control over their own distinct financial and risk management strategies.

Each company manages its own risks and policies within its “cell,” and the parent captive handles regulatory compliance.

How Do Cell Captive Insurance Companies Work?

Think of a cell captive as renting space in a shared building. While each business controls its own “cell,” the parent captive provides the structure, reducing costs and ensuring regulatory oversight. Cell captives allow more autonomy while sharing administrative overhead than group captives, which pools risks.

Benefits of Cell Captives

Your clients can see many benefits in choosing to go with a cell captive for their business.

- Cost Sharing: Since businesses share the overhead of running the captive, it reduces the financial burden, making it affordable for businesses spending $250,000 or more on insurance.

- Risk Customization: Each cell can customize its insurance policies based on the business's specific risks. This gives businesses more control over their policies than traditional insurance models, which provide one-size-fits-all coverage.

- Regulatory Flexibility: The parent captive manages compliance and reporting, reducing the burden on individual cell owners.

- Transparency and Control: Captive insurance offers a clearer view of premium allocation, giving businesses more say in risk management.

Drawbacks of Cell Captives

While your clients can see many potential benefits, cell captives aren't without their drawbacks.

- Limited Independence: While each business controls its cell, the parent captive dictates specific rules and governance. This can limit your ability to make decisions independently.

- Ongoing Fees: Businesses must invest in upfront costs and pay ongoing fees, which vary based on the structure and domicile of the parent captive.

- Shared Risk: While cells are insulated, there’s still indirect risk sharing through the overall structure. In some cases, you may share risk indirectly through regulatory or operational decisions made by the parent.

Who Are Cell Captive Insurers Ideal For?

Cell captives are best suited for businesses that:

- Spend at least $250,000 annually on insurance.

- Actively manage risk and seek control over insurance costs.

- Want transparency and customization without fully owning a captive.

Is a Cell Captive Right for Your Client?

Cell captives offer businesses a way to gain the benefits of a captive without the full investment of creating one. This model provides a compelling alternative for companies looking to control their insurance by sharing costs, customizing risk coverage, and enjoying regulatory flexibility.

But they’re just one option.

Explore our article on the pros and cons of single-parent and group captives to see which structure best fits your client's needs.

Do you think captives are right for your clients? Become a member of Captive Coalition for free. to access our tools, resources, webinars, training, and opportunities to help your best clients.

{kind=link}