You might want to know which type of captives would be ideal for your best clients. You might read the words “single-parent captive” and “group captive” and have an idea of what they mean with that limited context. But how does each type work? What are their pros? What are their cons?

Captive Coalition works specifically with captive insurers. We make understanding single-parent and group captives digestible for insurance agents and their clients. And we also find it important for you to learn about their pros and cons.

In this article, you’ll learn about the benefits and drawbacks of single-parent and group captives. That way, you can determine which type of captive insurer would benefit your client.

A Brief Overview of Captives

Captive insurance allows businesses to create their own insurance company. This approach offers greater control, potential cost savings, and the ability to customize coverage to fit specific needs.

|

Aspect |

Single-Parent Captive |

Group Captive |

|

Ownership |

Owned by one parent company |

Owned by multiple unrelated businesses |

|

Cost |

Higher initial setup but lower operational costs over time |

Lower individual costs due to shared expenses |

|

Risk Management |

Customized for one company’s risk |

Pooled risk management among members |

|

Regulatory Requirements |

Must meet individual state/domicile regulations |

Governed by group-specific regulations |

|

Flexibility |

Highly customizable |

Less flexible but still allows customization as long as it is confirmed to the group |

|

Capital Requirements |

Requires significant capital investment |

Lower capital requirements due to pooling |

|

Control |

Full control over policies and operations |

Shared control among member companies |

|

Benefits |

Potential for significant cost savings and control |

Cost-effective and shared risk management |

|

Fronting Carrier |

Typically required for regulatory compliance |

Typically required for regulatory compliance |

You might be wondering how your best clients would do in a captive in general. Take this captive assessment tool to get your results.

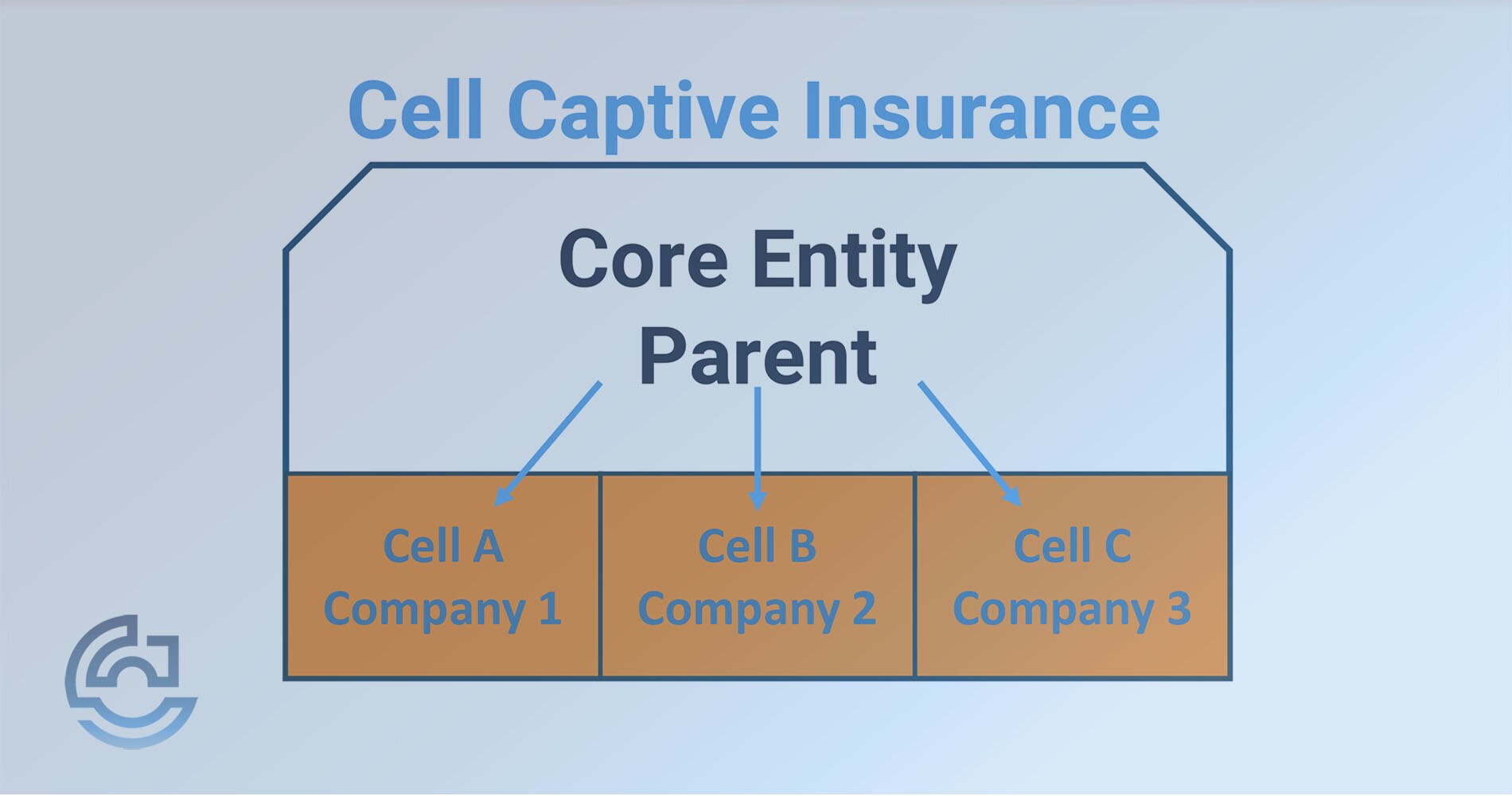

What is a Single Parent Captive Insurance Company?

A Single-Parent Captive is an insurance company owned by one parent company. This structure provides coverage for the risks of the parent company alone. The key benefits include:

- Control—The parent company has complete control over the insurance policies and operations. This allows for customization that aligns with the parent company’s specific risk profile and business needs.

- Customization—Policies can be customized to the exact requirements of the business, making it so their coverage is as effective and efficient as possible.

- Cost Savings—Potential for significant savings on insurance costs over time due to better risk management and fewer claims.

While these are excellent benefits for businesses, the downside is that single-parent captives require significant capital investment and have higher setup and operational costs.

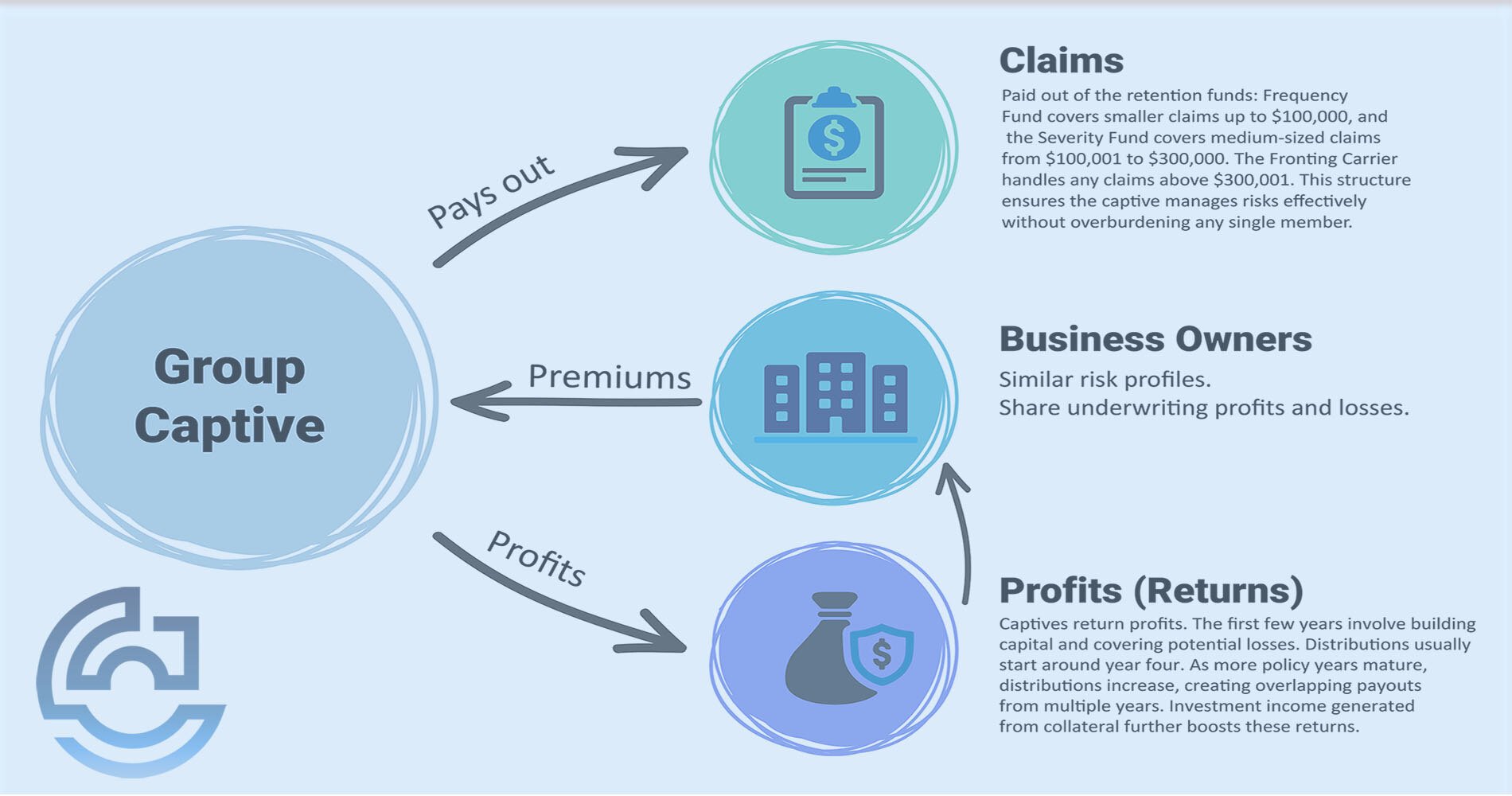

What is a Group Captive Insurance Company?

Group captives are shared insurance entities formed by multiple unrelated businesses that have similar risk profiles. These businesses pool their resources to collectively manage and underwrite their risks. The advantages of group captives include:

- Cost Efficiency—Shared expenses lead to lower individual costs, making this a cost-effective option for smaller businesses or those looking to reduce upfront expenses.

- Risk Sharing—Risk is pooled among other member businesses, providing collective stability and reduced volatility.

- Regulatory Simplicity—Group captives often follow group-specific regulations, which can streamline the compliance process.

Group captives involve shared control among the member businesses and are less flexible than single-parent captives, but they still offer significant customization options.

Comparing Single-Parent and Group Captive Costs

- Single-Parent Captives—Higher costs due to the need for substantial capital investment and individualized risk management.

The industry recommends a business spends at least $1 million on premiums before even considering a Single-Parent Captive. - Group Captives—Lower individual costs as expenses are shared among multiple members, reducing the financial burden on each participant.

The industry recommends a business spends at least $250,000 on premiums before joining a group captive.

Risk Management

- Single-Parent Captives—Customized risk management strategies specific to the parent company’s needs.

- Group Captives—Pooled risk management strategies that provide collective stability.

Regulatory Considerations

- Single-Parent Captives—Must comply with individual state regulations and reporting requirements, which vary depending on location.

- Group Captives—Governed by group-specific regulations agreed upon by all members, offering a more streamlined compliance process.

Benefits of Each Captive Insurer

- Single-Parent Captives—Significant control, potential cost savings, and premiums customized to the parent company’s needs. These captives will generate about 15% more underwriting profit.

- Group Captives—Cost-sharing benefits, reduced initial expenses, collective risk management.

Frequently Asked Questions (FAQs) About Captive Insurance

What is a Single-Parent Captive?

A Single-Parent Captive is an insurance company established by one business to insure its own risks, offering complete control and customization.

How does a Group Captive work?

A group captive is formed by multiple businesses to pool resources and manage their risks collectively, sharing the costs and benefits.

What are the cost differences between Single-Parent and Group Captives?

Single-parent captives require higher initial and operational costs, while group captives share expenses among members, reducing individual costs.

How do captives manage risk?

Single-parent captives customize risk management to one company’s needs, while group captives use pooled risk management among members.

What are the benefits of choosing a captive over traditional insurance?

Captives offer greater control, cost savings, transparency, and customized risk management compared to traditional insurance models.

What is a fronting carrier?

A fronting carrier is a licensed insurance company that issues policies on behalf of a captive insurer, ensuring regulatory compliance and facilitating claims processing.

Is a Single-Parent or Group Captive Right for Your Client?

Choosing between a single-parent captive and a group captive depends on your client’s needs, resources, and risk profiles. Single-parent captives offer complete control and customization but require significant investment. Group captives provide cost-sharing benefits and reduced individual expenses but involve shared control.

Next, read our article about the financial advantages and disadvantages of captives. That way, you and your client can weigh whether or not the advantages outweigh the disadvantages.

Interested in captives? Want to learn more? Become a member of Captive Coalition for free to access tools, resources, webinars, training, and opportunities to get your best clients into captives.

{kind=link}